The promise was simple: live like you do in the Mediterranean on a small pension and pay taxes on foreign income in a way that wasn’t too harsh. In 2024, that story changed quickly, and many people who wanted to retire in the sun are now having to redo their retirement maths from scratch.

From no taxes to full taxes

Portugal’s “non-habitual resident” program, or RNH, drew in thousands of foreign retirees including many from France, for more than ten years. At first, private pensions from other countries were not taxed, but later they were taxed at a flat rate of 10%. For a lot of middle-class couples, that meant they had several hundred euros more in their pockets each month.

The ladder has been pulled up for new arrivals since January 2024. Newcomers who are retiring to Portugal are no longer eligible for the RNH scheme. Instead, they are taxed at Portugal’s normal progressive income tax rates, which can go up to 48% and, in some cases, almost 53% when surcharges are added.

A lot of people didn’t see this sharp turn coming. Many people who wanted to move abroad had made plans based on detailed financial projections that they had made with the help of experts. It was clear what everyone wanted: rules that stayed the same and a deal that lasted a long time. The truth is that things are much less certain now.

Plans for retirement went wrong

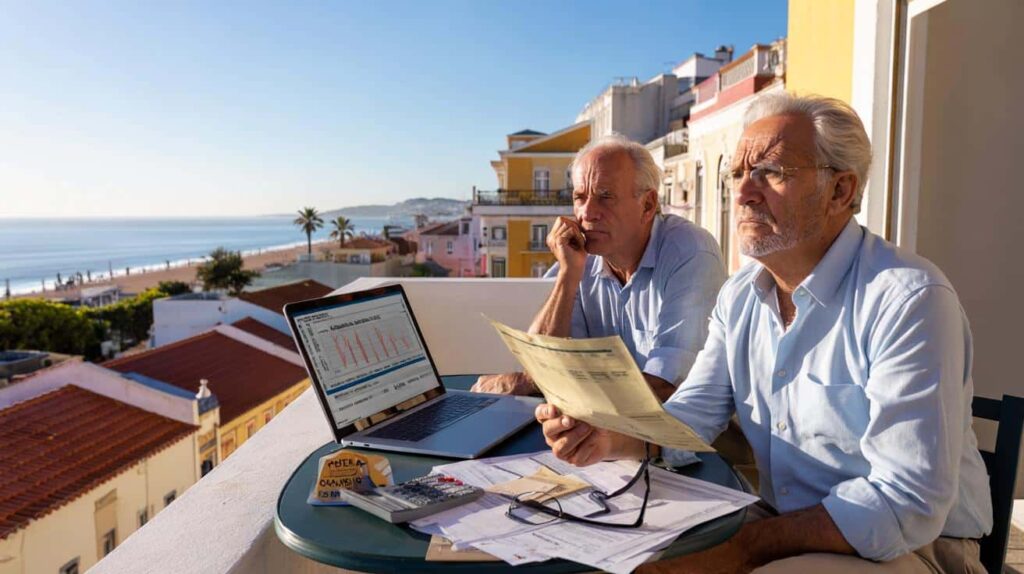

Portugal used to be the main attraction at French retirement and expat fairs. Couples sold their homes in Lyon, Lille, or Bordeaux, traded gardens for balconies near Faro or Lagos, and imagined their seventies spent walking on the beach and talking to their grandchildren on video calls.

A lot of those talks have changed tone. People who are retired talk about uncertainty and feeling stuck. It feels like the rules changed in the middle of the game. People who moved to a new country expecting one government now have to deal with another, and the cost of living, especially housing, has gone up a lot.

In the last ten years, property prices in popular Portuguese cities and along the coast have gone up a lot. Values shot up because more foreign buyers short-term rentals, and digital nomads were looking for homes. It costs a lot more now for pensioners to sell their homes and go back home or move to a cheaper country than it did when they first got there.

Why Portugal changed its mind

The government of Portugal says the change is a response to rising housing costs. People in Lisbon and Porto have been complaining for a long time about rising rents and the rise of tourist rentals, often blaming foreign investment and tax breaks.

The Bank of Portugal has warned many times about problems in the real estate market. Policymakers say that giving rich newcomers generous benefits was making an already hot market even hotter, while locals had trouble finding affordable housing.

The new policy is clear: tax breaks should be given to highly skilled workers and investments that make money, not to foreign pension income. There is a new plan in the works for some professionals, but retirees are not at the top of the list.

The new price of living in the sun

Income tax is just one part of the whole financial picture. New arrivals have to pay a number of extra Portuguese fees that can further cut into their pension income.

- A transfer tax on buying a home that goes up with the price of the home

- Annual property tax for cities, which varies by area and property value

- When you buy or import a car, you have to pay a lot of money in registration taxes.

- Road tolls and fuel taxes that add up quickly for people who drive a lot

For some things, like going out to eat at cheap restaurants buying basic groceries, or using local services, life can still feel cheaper than it does in France or the UK. But that gap has gotten smaller, especially in areas with a lot of tourists. Because new retirees have to pay more in income tax the overall budget may be tighter than expected.

A lot of retirees are now cutting back on non-essential expenses. You don’t go home for holidays as often. Renovation projects at home are taking longer than expected. Another recurring cost that puts a strain on fixed incomes is private health insurance, which is often bought along with access to Portugal’s public system.

Paperwork, language, and the secret side of being an expat

There is more to the situation than just the numbers. It can be hard to register with the tax authorities, sort out residency papers, declare foreign pensions, and deal with local banks, especially if you don’t speak Portuguese well.

Some retirees hire consultants or paid middlemen to help them deal with the red tape. That makes the budget even longer. Most people think that retirement will be less stressful than it is, but the first few years can be very stressful.

Spain, Morocco, Malta, and other places…

As Portugal tightens the tap, other places are suddenly more visible to retirees. Several countries around the Mediterranean and beyond advertise themselves as safe and tax-friendly places for foreign retirees to live.

| Country | What makes it appealing | Important thing to look out for |

|---|---|---|

| Spain | Cultural closeness, healthcare, and big communities of expats | Some areas have a wealth tax and different taxes in different regions. |

| Morocco | French is widely spoken, and the cost of living is lower. | Risk of changes in the exchange rate and different laws |

| Malta | English-speaking, certain pension plans | Rents are going up in a small housing market. |

| Cyprus | Warm climate and a good tax on foreign pensions | Political situation and distance from mainland Europe |

Advisers say that French and other European retirees who still want sunshine without a long-haul flight are more interested in Spain. Morocco is still a popular place for people who want to save money on daily expenses and be around people who speak French. Smaller countries like Malta and Cyprus set themselves apart with specific tax systems and lifestyle packages.

How the end of Portugal’s tax break changes choices

The Portuguese reform shows a basic truth about taxes across borders: governments can change their policies quickly, and often because of pressure from their own citizens. A decision made as part of a long-term plan can be changed if it becomes too expensive politically.

That means that people who are going to retire soon should look at more than just the headline tax rates. They should also think about the chance of sudden reform. Countries that have a history of changing their tax rates often may be less stable even if the current rates are good.

Running the numbers: a simple example

For example, a single retiree with a private pension of €25,000 a year. Under the old RNH system in Portugal, which had a flat tax of 10%, they could expect to keep about €22,500 before social charges and health care. This left them with enough money for rent daily expenses, and some travel.

With progressive taxation, the yearly take-home pay drops a lot, to about 30–35% on the same income. When rents go up in Lisbon or Porto, the benefits of living in a mid-sized French or British city mostly go away. In some cases, after paying for housing and health insurance, the retiree may be worse off than they were before they moved.

This is why advisers now tell people who want to move abroad to try out a few different situations the current tax rules, a version that is a little less favourable, and a worst-case scenario. The goal is not to guess what will happen in the future, but to see if your retirement plan is still possible if the rules change against you.

What else besides taxes makes a retirement abroad “good”?

People often think about moving because of tax savings, but these savings alone don’t usually make them move. Three things that usually make people happy in the long run are their living situation their ability to handle money, and their ability to plan ahead.

UK Ends Retirement at 67 Historic Shakeup Changes Pension Age and Sparks Nationwide Debate

UK Ends Retirement at 67 Historic Shakeup Changes Pension Age and Sparks Nationwide Debate

The living environment includes things like the weather safety healthcare, social life, and how easy it is to fit in. Financial resilience is being able to deal with changes in the value of money, rent going up, and surprise medical bills without giving up on the plan. Legal stability clear tax treaties with the home country, and the ability to understand official information without having to pay for help all the time make things more predictable.